When I last covered Coinbase (NASDAQ:COIN) for Seeking Alpha in April, I focused the article mainly on the performance of the company’s Ethereum (ETH-USD) scaling blockchain Base. Since Ethereum’s Dencun upgrade earlier this year, the Base blockchain has enjoyed explosive growth and has been one of the best performing secondary networks in the Ethereum ecosystem. In this update, we’ll look at the last few months of Base data compared with major L2 peers. We’ll also take a look at Coinbase’s transaction volume trend and assess what investors can likely expect for Q2 earnings to be released in August.

All About That Base, Still

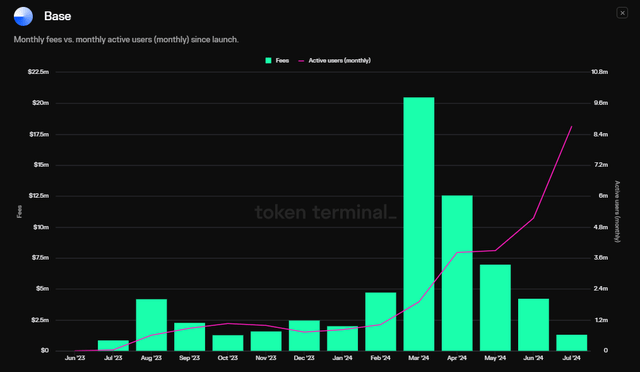

Base Fees for MAUs (Token Terminal)

March was an absolutely explosive month for the Base blockchain. The network generated over $20.5 million in fees. These fees are revenue that go almost entirely to COIN, as Coinbase is the only sequencer on the network. The company gives roughly 10% of that fee generation to the Optimism Collective. But the bottom line is Base usage is a good thing for Coinbase’s top line. Fees have admittedly been in decline since that initial post-Dencun spike earlier this year. During the second quarter, Base fees combined for $24.7 million. That said, Base is creating a somewhat sticky userbase with MAUs surging to 5.1 million for the month of June. This is up from just 1 million in February.

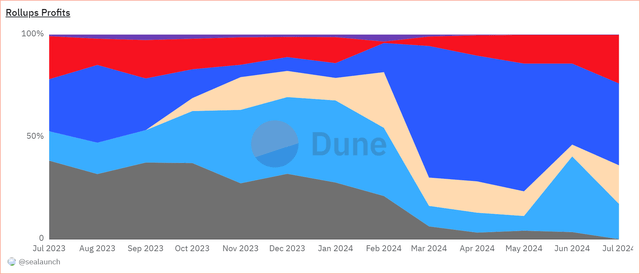

L2 Rollup Share by Month (Dune Analytics/sealaunch)

Despite ecosystem-wide declines in fees as the months have progressed post-Dencun, Base has continued to claim an “unfair” share of rollup profit. In both April and May, Base commanded over 60% of rollup profit. Since June, we’ve seen noticeable upticks in profit share from Arbitrum and Optimism, but base has still maintained about 40% of rollup profit share going back to the last 7 weeks.

Earnings & Volume

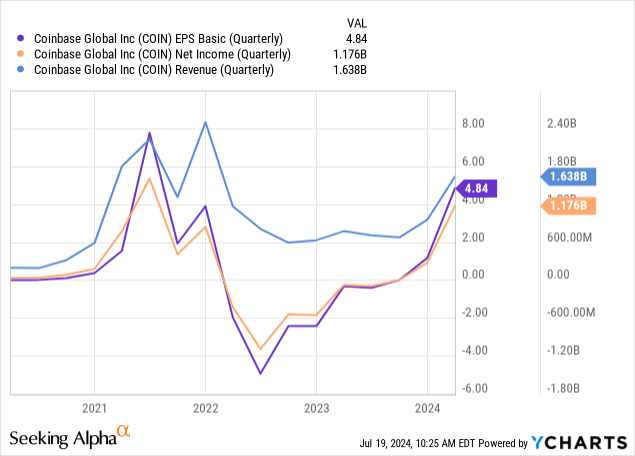

By just about any important financial metric, Coinbase had a phenomenal quarter in Q1-24. At $1.6 billion in revenue and nearly $1.2 billion in net income, the company had its best quarter since 2021. This performance was driven largely by an absolute surge in transaction volume in the first three months of the year:

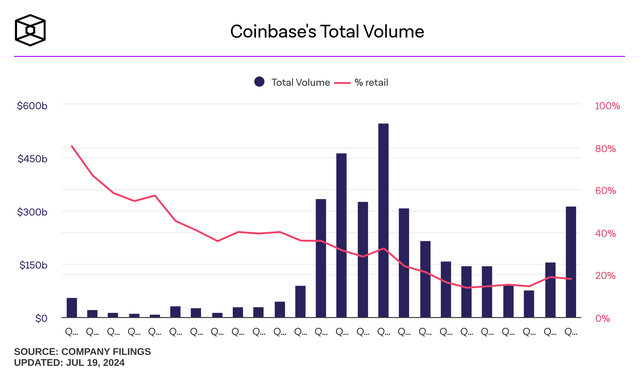

Coinbase Quarterly Volume (The Block)

Coinbase’s $312 billion in Q1-24 volume was its best three month period since Q4-21. Interestingly, retail share of volume has largely been in freefall over that same period of time from 32.3% down to just 18% in the last quarter. This is potentially problematic for Coinbase because the margin on retail trading is so much better than that of institutions. The company generally earns somewhere between 1.7-2.5% on its retail trading business yet just a few bps on its institutional volume.

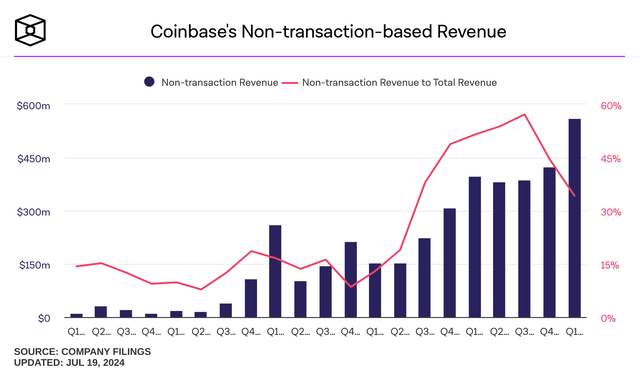

Non-Tx Revenue (The Block)

The company has done a nice job of growing non-transaction based revenue over the last several years. It has achieved this through growth in subscriptions, blockchain rewards, and interest income. These smaller but important business lines can help the company alleviate the cyclicality of its primary revenue driver.

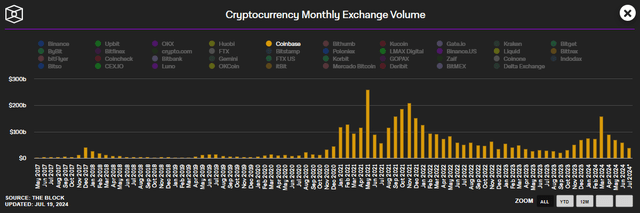

Coinbase Monthly Vol (The Block)

Looking ahead to the company’s Q2 report, exchange volume is likely to decline by roughly 30% quarter over quarter. Data from The Block shows $218.9 billion in total exchange volume for Coinbase between April and June.

Short Interest & Seasonality

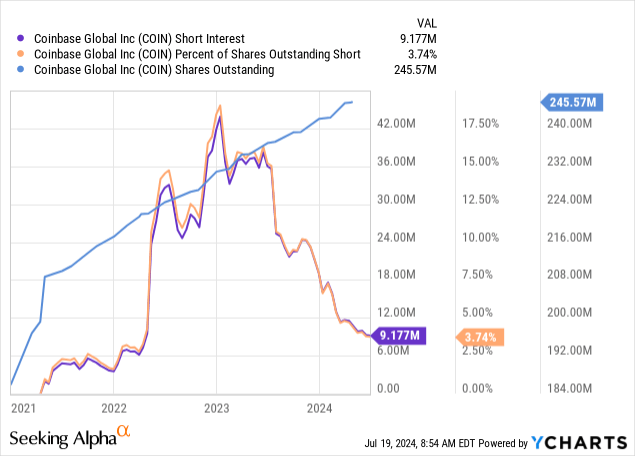

As a stock that benefits from a highly risky industry, Coinbase has had a very large short position in the past; highlighted by about a 12-month period between June of 2022 and 2023. Since then, both short interest expressed through number of shares and short interest as a percent of shares outstanding has been in decline:

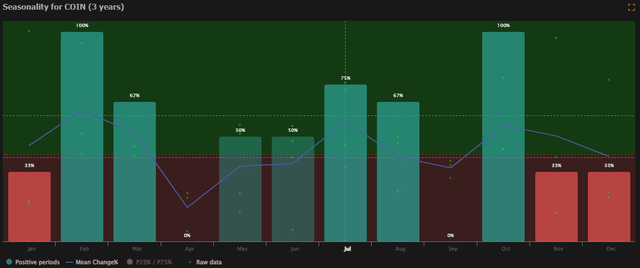

Today, we see the short interest as a percent of the outstanding shares down to just 3.7%. For all intents and purposes, the squeeze rally is seemingly over. That said, there may be a seasonal component to how the market views Coinbase. July has historically been one of the better months for COIN stock, with a mean change of over 15% over the last three years.

COIN Seasonality (TrendSpider)

August has generally been a bit more mixed for COIN historically, with a mean return of -1.2% despite positive returns in two out of three instances in the sample. What will certainly make a difference in COIN’s performance through the rest of the year is how much cryptocurrencies are rallying.

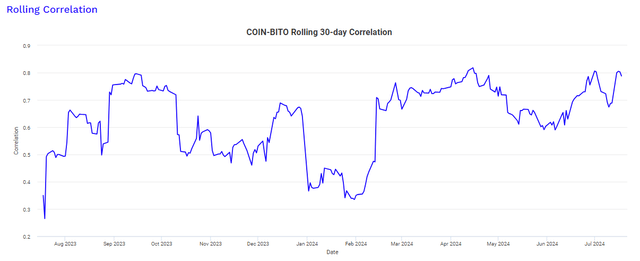

12 Month Correlation (PortfolioVisualizer)

Over the last twelve months, COIN has had a 65% correlation with the ProShares Bitcoin Strategy ETF (BITO) compared with just a 41% correlation with the S&P 500. Because of the margin Coinbase gets on retail trading compared to what it charges institutions, Coinbase benefits more from retail buying during FOMO rallies in Bitcoin (BTC-USD) and other cryptocurrencies rather than from the revenue it generates from institutional buyers.

Tx Margin (Filings, Author’s calculations)

Given this, the spot Bitcoin ETFs are a bit of a double-edged sword for COIN because it’s actually cheaper to buy BTC through ETFs than it is to own it on the exchange or in self-custody if one is simply buying for short to medium term speculation. This is a concept I explored recently.

Valuation

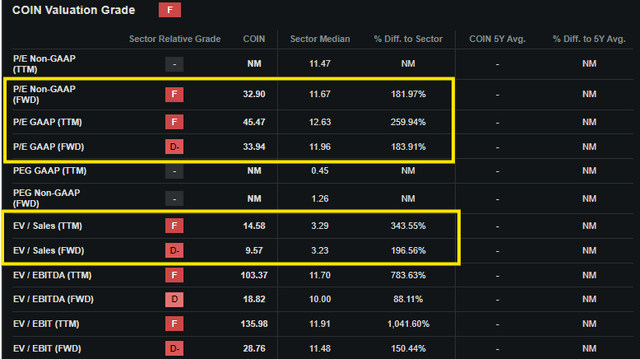

Depending on what your views are about the validity of blockchain-based digital assets or cryptocurrencies as investable assets, another important detail investors must be mindful of is the price they’re willing to pay for a company. Even as someone who holds the view that digital assets and public blockchains have a bright future, I still don’t know that I can justify paying 34x forward earnings and 10x forward sales to buy COIN:

COIN Value Grades (Seeking Alpha)

This screenshot shows just a few of the multiples COIN shareholders are paying to own the stock. But based on just about every metric that Seeking Alpha tracks when building its overall Valuation Grade, COIN scores a D- or F. Coinbase may indeed benefit from long-term growth in sequencer fees, centralized exchange volume, and non-transaction based revenue. But it’s difficult to argue that it hasn’t been priced in already.

Closing Thoughts

Even with an improving regulatory environment for the crypto industry in the United States, it’s difficult for me to justify buying COIN at these valuations. I see several potential headwinds for the company’s flagship transaction business, and I’ve elaborated on those headwinds in past articles; namely, decentralized exchanges on-chain will potentially cannibalize centralized exchange transaction volume as they grow share of the market. Additionally, if retail BTC traders start doing more of their trading through ETFs rather than exchanges, Coinbase is swapping high margin business for low margin business even if it’s the custodian of the ETF assets. All this said, shorting a company that is so highly correlated with Bitcoin is a dangerous game to play. I still think COIN is a hold today.

Read the full article here