Broad global trends

Favorable outlook for monetary easing

- Across global geographies, managers are expecting central banks to reduce interest rates. This paints a positive outlook for more cyclical, value-oriented names – and managers are incrementally increasing exposure to such positions. These include companies in autos, transportation, and short-cycle industrials.

- With the looming possibility of rate cuts, many managers are looking at opportunities within the banking sector in Europe and the U.S., given highly attractive valuations and the increased potential for loan growth stemming from lower borrowing rates.

The AI-related opportunity set is evolving

- Investors continue to be bullish around artificial intelligence (AI)-related opportunities, but are beginning to favor service providers versus infrastructure-driven plays. While most managers expect the AI infrastructure buildout to continue, growth rates in capital expenditures may decline if AI application development does not keep pace with installed capacity, leading to potential underperformance in capex-driven stocks.

- Managers are also more optimistic about consumer products and service companies with AI-enhanced capabilities. This includes consumer electronics companies that are developing products with pending AI features.

Opportunities in Europe and the UK

- Easing inflation and rate cuts are expected to provide a favorable tailwind for European equities, with smaller cap companies representing a particularly compelling opportunity. U.S.-based long-short equity funds have recognized the opportunity, as they’ve been buyers of European equities for eight consecutive months and have the highest net exposure since 2010.

- The UK provides a ripe environment for mergers and acquisitions (M&A) activity, which has the potential to drive multiple expansion from low valuations.

Evolving environment in emerging markets

- While the U.S. dollar (USD) strength has delayed rate cuts in many emerging markets (EM) countries that have opted to defend their currencies, such as Brazil and Mexico, managers believe that expectations for monetary easing should provide an economic tailwind.

- Sentiment on China remains mixed, although there are signs of improving consumer sentiment, particularly within the travel segment. Many Chinese companies are also seeking to boost shareholder returns through dividends and share buybacks.

Continued bullishness in commodities

- The outlook for copper continues to be very bullish due to demand stemming from data centers and increased electrification. Natural gas is also gaining interest due to reduced supply and increasing demand for energy production related to data centers.

Global equities

Technological diffusion of AI impact

- Investors are increasingly constructive on new replacement cycles in the consumer electronics space with pending AI features.

- Less-hyped software providers that leverage generative AI for scalability are attractive relative to more expensive AI chipmakers.

- Conversely, some managers are monitoring capex expenditure levels and the potential overcapacity of data centers.

Market volatility will redraw the landscape

- Anticipating some market noise around presidential elections, U.S. Federal Reserve (Fed) rate expectations, and geopolitical risks, value investors are looking toward opportunities in overlooked cyclicals such as autos, airlines, and depressed durable businesses such as special chemicals, utilities, and agriculture.

- That said, managers are wary of weak consumers, and are avoiding areas such as discount stores, preferring consumer financials.

- Given the increasing market uncertainty, some managers are taking profits in cyclicals that performed strongly over the past year, i.e., energy stocks.

European banks gain consensus as bargain buys

- Growth managers, akin to value managers, are increasingly positive on European banks given higher interest rate trends, net interest margins, and attractive valuations relative to their U.S. peers.

Obesity drugs move from concept to clear adoption

- Managers are adding to GLP-1s given the increasing visibility of growth of such treatments. This is based on evidence of increasing prescriptions and market popularity.

Corporate governance remains a path to higher returns in Japan

- Low valuations, visible corporate governance improvements, and a cheap Japanese yen are drawing both growth and value investors toward unloved industrial conglomerates in Japan.

U.S. equities

Not all AI is created equal

- Active equity managers are increasingly differentiating between AI companies, shifting exposures toward service providers and away from capital spending plays.

- While most managers expect the AI infrastructure buildout to continue, growth rates in capex may decline if AI application development does not keep pace with installed capacity, leading to potential underperformance in capex-driven stocks.

- Value managers are adding to companies with large AI-enhanced advertising businesses such as Amazon and Meta, while growth managers are upping holdings in companies like Apple that could benefit from a shift in AI apps to devices.

Interest rate cuts to the rescue?

- Markets are currently expecting with near-certainty that the Fed will begin cutting interest rates in September. Following the typical historical playbook, managers are increasing exposure to value-oriented and smaller cap stocks.

- Within value, managers are adding to positions in early cyclicals such as transportation, short-cycle industrials, and automotive names, as well as smaller-cap companies.

- Dedicated small cap managers are tilting portfolios toward financials (particularly banks), technology, and more highly indebted companies that will benefit from lower rates.

Positioning ahead of the election

- Recent events brought notable shifts in the odds for party control of the U.S. presidency and Congress. Most managers view political outcomes as inherently unpredictable or swiftly discounted and in general refrain from taking explicit bets.

- That said, companies in industries likely to benefit under either party control, such as construction, are favored. On the other hand, companies within the consumer discretionary sector like retailers, which could be hurt by higher tariffs, are consensus underweights.

Emerging markets equities

Attractiveness of emerging markets persists

- The improved macroeconomic environment and capacity for monetary policy easing continues to be a favorable backdrop for growth in emerging markets (EM).

- Valuation spreads within the EM opportunity set remain wide in a historical context. The anticipated positive inflection in earnings could provide compelling conditions for skilled active managers.

- The U.S. elections are expected to further drive volatility and create attractive entry points for long-term investors. Additionally, EM continues to be under-owned, so renewed interest could drive inflows and re-rating.

Currency weakness seen as temporary

- The USD strength has delayed rate cuts by central banks in EM, such as Brazil and Mexico, which have opted to defend their currencies. Investors expect these cuts to materialize in the second half of 2024, benefiting these economies.

- In addition, post-election volatility in Brazil has created attractive valuation openings for investors who remain committed to the opportunity set within Brazilian financials and consumer names.

Tailwinds for China despite mixed sentiment

- Investor sentiment on China remains mixed. While consumer-related sectors remain weak, signs of improvement are emerging in the travel sector, with strong air travel and hotel bookings. Elsewhere, investors continue to be attracted to valuations in growth names.

- Akin to Japan and Korea, China is emphasizing shareholder returns through dividends and share buybacks, which have been a tailwind, particularly for state-owned enterprises.

Managers continue to be attracted to India

- Post-election government and private capital expenditures are expected to support existing growth expectations.

- Moreover, some investors believe demographic tailwinds, labor pool availability, and infrastructure investments will continue to drive strong economic growth in India, but see these as underappreciated by the market.

Long/short equity

U.S.-based hedge funds overweight Europe

- Elevated European Union (EU) exposure: U.S.-based hedge funds have been net buyers of European equities for eight consecutive months, pushing their net exposure to the highest levels since 2010.

Easing momentum tilts and shifting exposures

- Continued selling in the Magnificent Seven group of stocks, AI beneficiaries, and the momentum factor: Hedge funds were net sellers of both the Magnificent Seven and AI beneficiaries, with the selling in the Magnificent Seven being the largest seen since early February. Long/short tilts in both the Magnificent Seven and AI beneficiaries are at the lowest levels observed over the last 12 months. This has led to a moderation in hedge fund exposure to momentum stocks.

Elevated gross leverage with lower beta/volatility profile

- High gross leverage: Gross leverage remains near recent peaks and above 200%, which historically would suggest an upcoming de-grossing event based on seasonal trends.

- Lower risk profile: However, when adjusting for the beta of the holdings, the beta-adjusted gross leverage is significantly lower in relative terms, sitting in just the 54th percentage tile. This indicates that hedge funds have been avoiding high-beta shorts and rotating out of some of the higher-beta AI winners, reducing the overall risk profile of their portfolios.

Europe and UK equities

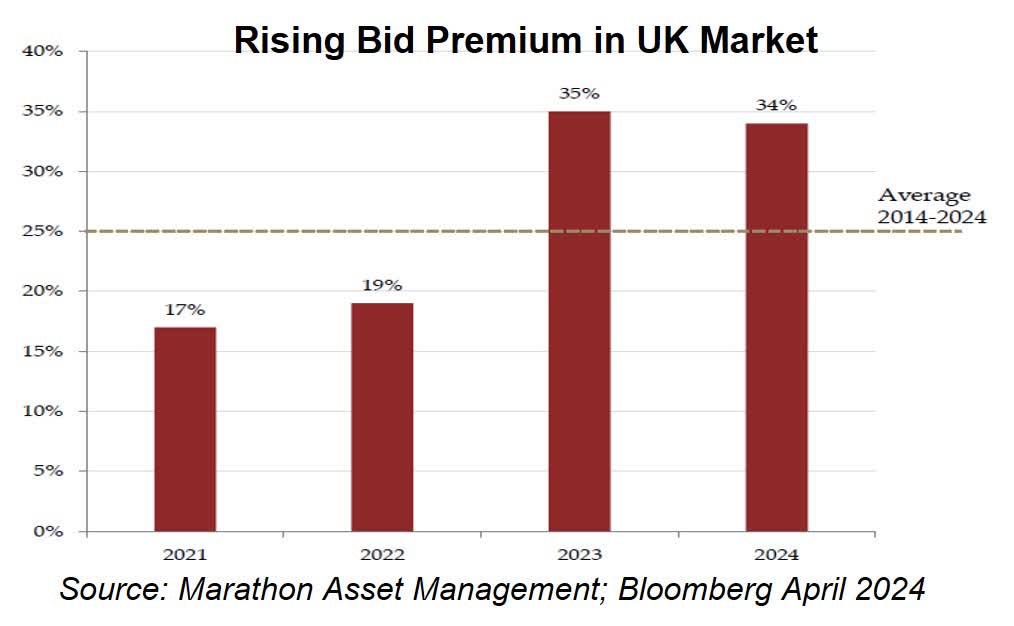

- The UK market is attracting increasing takeover interest. The market’s low valuations mean that recent bids are coming at high bid premia. This activity has the potential to be the catalyst to crystalize the value which has long been apparent in the UK market.

- After three years of underperformance, European small cap equity valuations are at 10-year lows relative to history and their large cap peers. Historically, European small caps have rebounded 50% relative to European large caps in the first year after bottoming out. We believe that easing inflation and potential rate cuts later this year and in 2025 could be the catalysts for a rebound.

Japan equities

Increasing interest in laggard stocks

- Japan’s mega-cap stocks continued to outperform last quarter, supported by further yen depreciation. However, rising expectations of a Fed rate cut, which could lead to yen appreciation, have led an increasing number of managers to expect the mega-cap rally to end. Many mega-cap stocks have overseas exposures.

- Many value managers are shifting into defensive stocks, such as consumer staples and/or telecommunications, which lagged in the up market.

- Many growth managers are shifting into laggard stocks in the electronics sector, anticipating a broadening effect of generative AI enhancements in addition to a cyclical recovery. Some managers are also increasing exposure to small-cap growth stocks, whose valuations have become more attractive due to significant underperformance in the past.

Improving sentiment on Japan’s domestic consumption

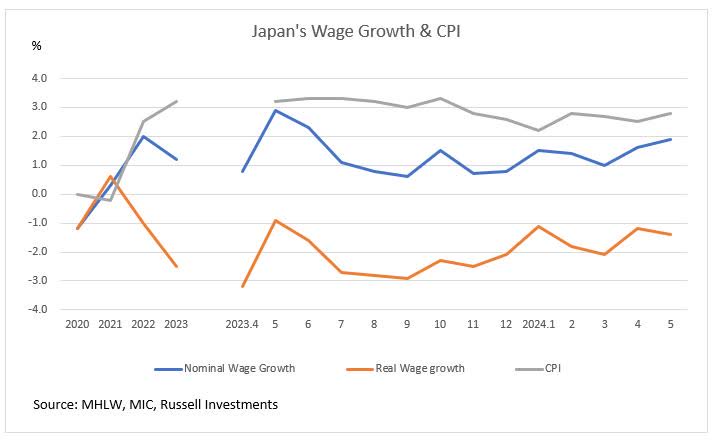

- While household consumption has remained weak, an increasing number of managers expect domestic consumption to recover, thanks to anticipated real wage growth backed by the stabilization of the CPI (consumer price index).

- These managers are interested in buying domestic demand-driven names, such as retailers or consumer staples and services.

Canadian equities

Constructive view on commodities

- Copper: Managers maintain their bullish stance on copper over the intermediate to long term. They anticipate a supply-demand mismatch, with copper supply entering a shortage period while demand remains strong, driven by increasing electrification of the energy grid and demand for data centers due to generative AI.

- Natural gas: Similarly, managers hold a positive long-term view on natural gas. Prices have surged in the quarter following reduced U.S. production. The increasing demand for data centers, which require reliable and affordable energy, provides additional support for their long-term positive outlook.

- Gold: Gold prices continue to reach all-time high levels, driven by various factors including global geopolitical risks and interest-rate cut expectations by central banks. Managers are starting to see potential for positive inflection in mining company margins.

Opportunities within financials

- Within financials, the sentiment around Canadian banks has turned more cautious as revenues are slowing and credit losses are trending higher.

- Some active managers believe the long-standing negative sentiment on life insurance companies is shifting since the interest-rate regime moved away from a zero interest-rate environment. They believe this can present structural rerating opportunities in the life insurance space.

Interest rate moves and real estate

- The Bank of Canada kicked off its easing monetary policy in the second quarter, and followed up with a second rate cut in July. The back-to-back cuts could spur some revival in the real estate market, a sector that is very sensitive to interest rate changes. That said, while there is some easing, borrowing costs remain high relative to pre-pandemic levels.

Australian equities

Inflation still a concern

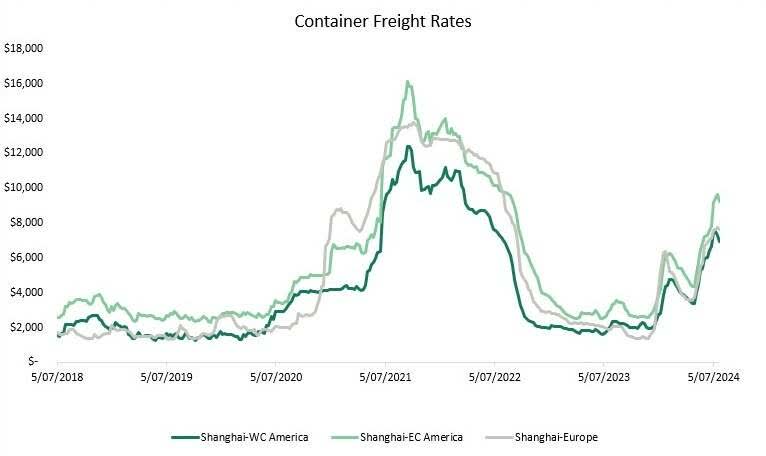

- Managers believe inflation remains a risk to company earnings, due to both domestic and global factors. In Australia, labor costs are expected to continue to rise. Freight costs are also anticipated to climb due to the disruption to global shipping channels caused by the conflict in the Middle East.

- Managers are preferring companies which have higher margins to withstand increased costs, and are lowly geared.

Source: Firetrail, Bloomberg

Consumer bifurcation

- Managers note that while the overall Australian consumer is robust, there is a significant divergence of financial health within the population. Wealthier and older Australians have increased their spending due to the benefits of higher interest earnings and asset growth, while younger and lower-income individuals are reducing their spending as the rising cost of living dampens their purchasing power.

- This bifurcation impacts stock selection, with managers preferring companies which can either benefit from it—i.e., the travel sector—or can manage reduced demand. Well-managed companies in essential goods, such as utilities and supermarkets, are also favored.

Real assets

Listed vs. non-listed: Valuations and debt maturities in focus

- Private real estate continues to trade at higher valuations than public REITs (real estate investment trusts). Investors view REITs as attractive.

- Private investors are lining up dry powder to deploy in 2025 and 2026, as they believe write-downs have close to bottomed out and macroeconomic fundamentals should become a tailwind.

- Debt maturities will be in focus as refinancing headwinds are likely to be a drag on earnings in both listed and non-listed real estate.

Real estate: Reaching a turning point?

- Investors are optimistic on REITs entering the second half of 2024. They currently trade below their net asset values, and valuations remain cheap relative to broad equities. Falling interest rates are expected to become a tailwind to performance.

- Investors expect positive earnings growth, and balance sheets remain strong.

- Demand remains healthy, speaking to strong bottom-up fundamentals. Managers are in a position to become more aggressive moving forward.

- Increased home ownership costs and demographic trends support single family rentals.

- Data centers continue to be an area of focus for managers, as acceleration in demand has led to record absorption.

Infrastructure: Benefitting from delayed rate cuts

- Decelerating economic growth and sticky inflation should continue to benefit infrastructure in the second half of 2024.

- Power demand is set to increase significantly in the coming years. Utilities companies have increased their load growth forecasts to account for new demand.

- New demand should increase base rates and further accelerate EPS (earnings per share) growth, but regulatory measures have the potential to hold back growth.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the “FTSE RUSSELL” brand.

The Russell logo is a trademark and service mark of Russell Investments.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

CORP-12566

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here