BorgWarner Inc. (NYSE:BWA) delivered optimistic guidance for the year 2023, and expects to launch a spin-off transaction, which may enhance stock price dynamics. Also, with the recently announced expansion of the South Carolina facility and the bet in the EV market, in my view, capacity increase could lead to sales growth. There are risks from the total amount of debt and M&A integration, however I believe that the stock could trade at higher marks.

BorgWarner

Currently, the automotive industry is changing at an ever-increasing pace. Mega trends like autonomous driving connectivity, rideshare, and cleaner driving are receiving a lot of attention from investors. No matter what the mode of transportation is, there is always the need for an efficient propulsion system. BorgWarner has been at the forefront of these technologies for over a century. The company designs innovative mobility technologies that reduce energy consumption and emissions while improving performance.

Source: Corporate Website

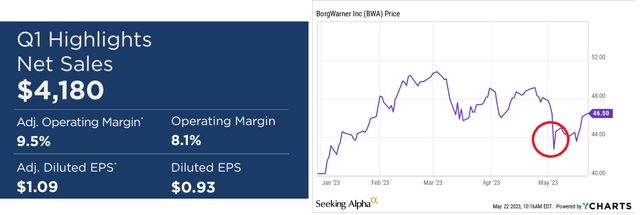

With that about the business model, I believe that the recent mixed quarterly results reported represent a great opportunity to have a look at the current fair valuation of the company. I wonder whether the recent decline in the share price is fully justified. In Q1 2023, the company reported net sales of $4.18 billion, adjusted operating margin of 9.5%, operating margin of 8.1%, and diluted earnings per share close to $0.93 dollars.

Source: Q1 2023 Results

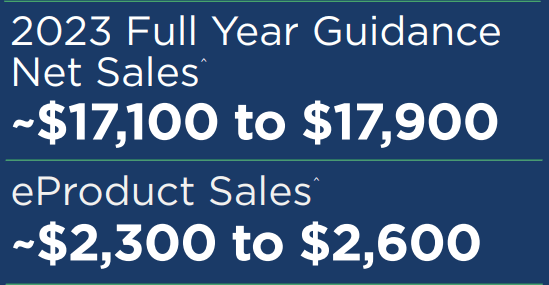

I believe that the guidance was pretty much beneficial for the company. Management reported 2023 full year net sales of $17 billion with eProduct sales of around $2.3 billion.

Source: Q1 2023 Results

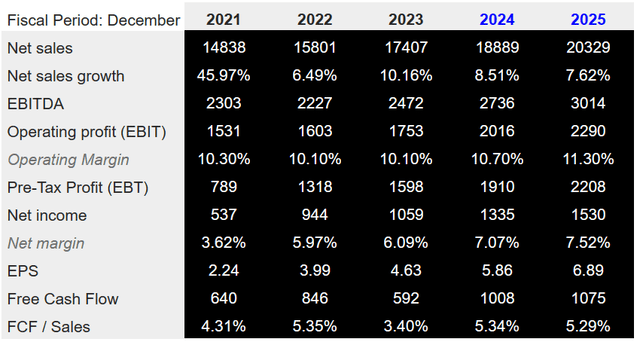

It is also worth considering that many analysts are expecting sales growth in 2024 and 2025, along with increases in pre-tax profit and net margin growth in 2024 and 2025. Besides, the free cash flow is expected to reach close to $1.008 billion in 2024 and $1.075 billion in 2025. Considering the free cash flow generation growth, I expect much more optimism in the market in the coming years.

Source: S&P

The Tax-free Spin-Off Could Enhance The Stock Price

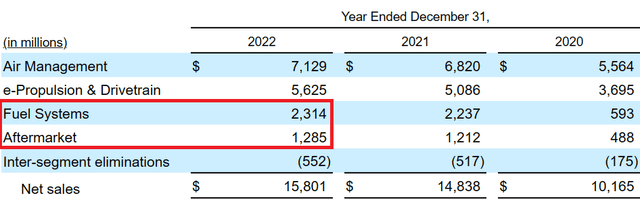

In my view, investors should have a look at the tax-free spin-off of Fuel Systems and Aftermarket segments announced in December 2022. Considering the current valuation of the company and the valuation of electric vehicle companies, the spin-off may make the whole corporation a bit more valuable.

On December 6, 2022, we announced our intention to execute a tax-free spin-off of our Fuel Systems and Aftermarket segments into a separate, publicly traded company. The intended separation of our Fuel Systems and Aftermarket segments would be an important next step in furthering our pivot to EV and advancing our vision of a clean, energy-efficient world, while at the same time creating a new, focused company with strong financials to support the new company’s future. Source: 10-k

The transaction is expected to be completed by the end of the third quarter of 2023, so I believe that we may see an improvement in the valuation in the coming months. Just to put things a bit in perspective, the full systems segment reported more than $2 billion in sales in 2022, and the aftermarket segment reported more than $1 billion in the same period. The transaction appears quite ambitious.

The Company expects to complete the transaction by the end of the third quarter of 2023, subject to satisfaction of customary conditions. Source: 10-k

Source: 10-k

Balance Sheet

In the last quarterly balance sheet, management reported an impressive increase in the total amount of assets driven by increases in account receivables, increase in inventories, and increases in payments and other core assets. Considering that total liabilities did not increase in the same period, I believe that the balance sheet is moving in the right direction.

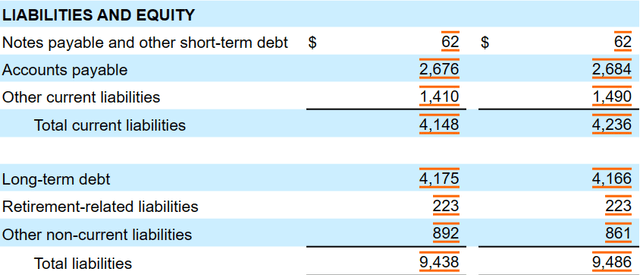

As of March 31, 2023, BorgWarner Inc. reported cash, cash equivalents, and restricted cash of close to $950 million, with accounts receivables of $3.566 billion, inventories close to $1.8 billion, prepayments and other current assets of $291 million, and total current assets of $6.607 billion. The total amount of current assets is larger than the total amount of current liabilities, so I wouldn’t be worried about the total amount of liquidity.

Property, plant and equipment are equal to $4.463 billion, with investments and long-term receivables worth $895 million and goodwill of $3.420 billion. Finally, total assets stand at $17.11 million, implying an asset/liability ratio close to 2x.

Source: 10-Q

With regards to the total amount of liabilities, BorgWarner reported notes payable and other short-term debt close to $62 million, accounts payable of $2.676 billion, and other current liabilities worth $1.410 billion. Also, with long-term debt of $4.175 billion and retirement-related liabilities close to $223 million, total liabilities stood at $9.438 billion.

Source: 10-Q

DCF Model

I assumed that investors will likely choose BorgWarner for the new focus of improving fuel economy and reducing emissions. At the end of the day, there are a lot of clever individuals inside BorgWarner Inc., which will likely offer a lot of relevant information for the new EV ventures.

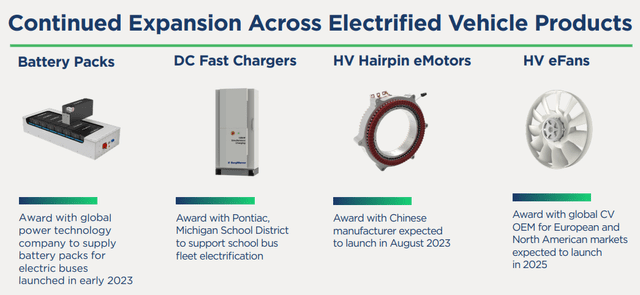

In my opinion, if management continues to expand across electrified vehicle products like battery packs or DC fast chargers, I believe that the demand for these products will likely bring revenue growth and free cash flow growth in the coming years.

Source: Q1 2023 Results

Besides, further expansion of existing facilities for battery back production like the one in South Carolina will likely increase the capacity, and may bring revenue growth. I think that further information and communication about the South Carolina facility, which is expected to be completed in Q2 2024, will likely bring demand for the stock.

Source: Q1 2023 Results

It is also worth noting that employees have developed partnerships with customers and suppliers to gain a deeper understanding of their challenges as well as to help them find the solutions to build vehicles that support a cleaner, more energy efficient world. I believe that these partnerships will likely help BorgWarner in the future. In addition, these partnerships will likely represent a barrier to entry for new competitors in the electrical vehicle industry.

The company is targeting close to 45% of total revenue from electric vehicles by 2030. In my view, investors looking for companies fully invested in EVs will most likely find the initiative quite interesting. As a result, we may see an increase in the demand for the stock, which may accelerate the stock price dynamics.

We are targeting revenue from products for pure electric vehicles to be over 25% of total revenue by 2025 and approximately 45% of total revenue by 2030. Source: 10-k

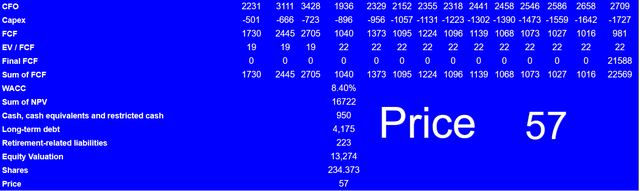

My DCF model includes 2023 net earnings of $3.846 billion, depreciation and tooling amortization close to $1.172 billion, other non-cash adjustments close to -$114 million, and retirement plan contributions of -$58 million. Besides, I included 2033 changes in receivables of -$4.208 billion, changes in inventories of -$969 million, and accounts payable and accrued expenses close to $2.179 billion.

Source: My DCF Model

I also assumed prepaid taxes and income taxes payable of around $293 million. Finally, my model also included a CFO of $2.708 billion, capital expenditures of -$1.728 billion, and 2033 FCF of $981 million.

Source: My DCF Model

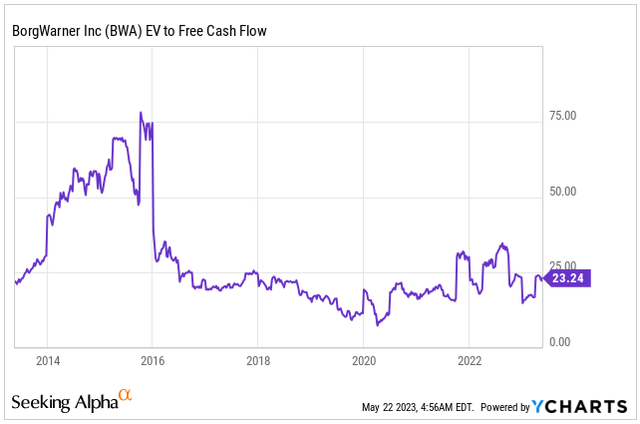

Have a look at the chart below to see that the EV/FCF stood at close to 74x in the past, and it is now close to 22x-23x. If we assume an EV/FCF multiple of 22x, which I believe is quite conservative, the final 2033 FCF would be close to $21.588 billion. With a WACC of 8.4%, the implied net present value would be close to $16.721 billion.

Source: Ycharts

If we add cash, cash equivalents, and restricted cash of around $950 million, and subtract long-term debt of $4.175 billion and retirement-related liabilities of $223 million, the implied equity valuation would be $13.273 billion. Finally, the implied fair price would be $57 per share.

Source: My DCF Model

Risks

If BorgWarner fails to deliver the revenue expected because the new products do not reach the expectations of the market, or the company suffers lack of necessary raw materials, the stock price will likely decline. Management also noted that lack of innovation or new adequate technologies could make the products obsolete. In this regard, I believe that investors may want to have a look at the lines below.

We may not meet our goals due to many factors, including any of the risks identified in the paragraph that follows, failure to develop new products that our customers will purchase, and technology changes that could render our products obsolete, or the introduction of new technology to which we do not have access, among other things. Source: 10-k

Considering the spin-off expected and recent acquisitions, I believe that sale of certain internal combustion assets is likely. If management fails to obtain decent valuations for the assets sold, I believe that the total amount of assets could decline. Such failures may bring the attention of shareholders, who may decide to sell shares.

Additionally, there is no certainty that we will be able to dispose of certain internal combustion assets on favorable terms, if at all, and the disposition process is expected to consume significant management resources. Source: 10-k

The total amount of debt is substantial, which may explain the new spin-off and the recent reorganization of the business model. Most payments are expected for 2025, 2026, and 2027, so I believe that negotiation with debt holders will likely be possible. With that, in my opinion, deterioration in the credit markets or further increase in the interest rates may lead to lower FCF growth and lower stock valuation.

Source: 10-k

Conclusion

BorgWarner Inc. delivered beneficial guidance for the year 2023. Management recently noted that the South Carolina facility will start a new expansion process in Q2 2023. I believe that further expansion of capacity, more exposure to the EV market, and the recent spin-off expected in 2023 will likely lead to stock appreciation. There are obvious risks from the total amount of debt, obsolescence of certain products, failed M&A integration, or lower FCF than expected. With that, I believe that the stock price could trade at a higher mark.

")